- Our Blog

Download PDF

Equity compensation awards have become available to more employees in the past couple years. How can advisors help their clients get the most out of them?

An asset that’s often misunderstood

While equity awards are a big component of compensation for pre-IPO companies, they’re also increasingly offered to a broader set of employees at dynamic publicly held companies. This trend can create significant opportunities for advisors to add value to a growing segment of clients — many of them younger and in need of long-term planning.

Our experience with employees receiving stock awards is that many of them don't understand the basics of this type of compensation.

Advisors can add value to their clients with equity compensation in three key ways:

- Educate them on how equity compensation works, including implications for taxes and portfolio allocation.

- Help them understand the details of their specific plans and holdings.

- Develop strategies for tax optimization and risk management.

Framing the conversation: Talking to pre-IPO clients

Company stock awards will, in most instances, count as W2 income along with base wages and bonus cash compensation.1 As W2 income, awards are subject to both income tax and payroll tax withholding. But unlike cash compensation, they are deposited in the employee’s brokerage account, not their bank account, which is one reason why this type of compensation is misunderstood.

Once it’s acquired, the stock can be viewed as an investment, but one that almost always comes with limitations. For example, there are usually restrictions on the transferability of the stock before an event like an initial public offering, making it difficult or impossible to liquidate. And even after the company goes public, there may be plan-imposed controls such as lockup and blackout periods, holding requirements and limits on hedging or using the stock as collateral for a loan. All these factors inform decisions on when and how much to hold or sell.

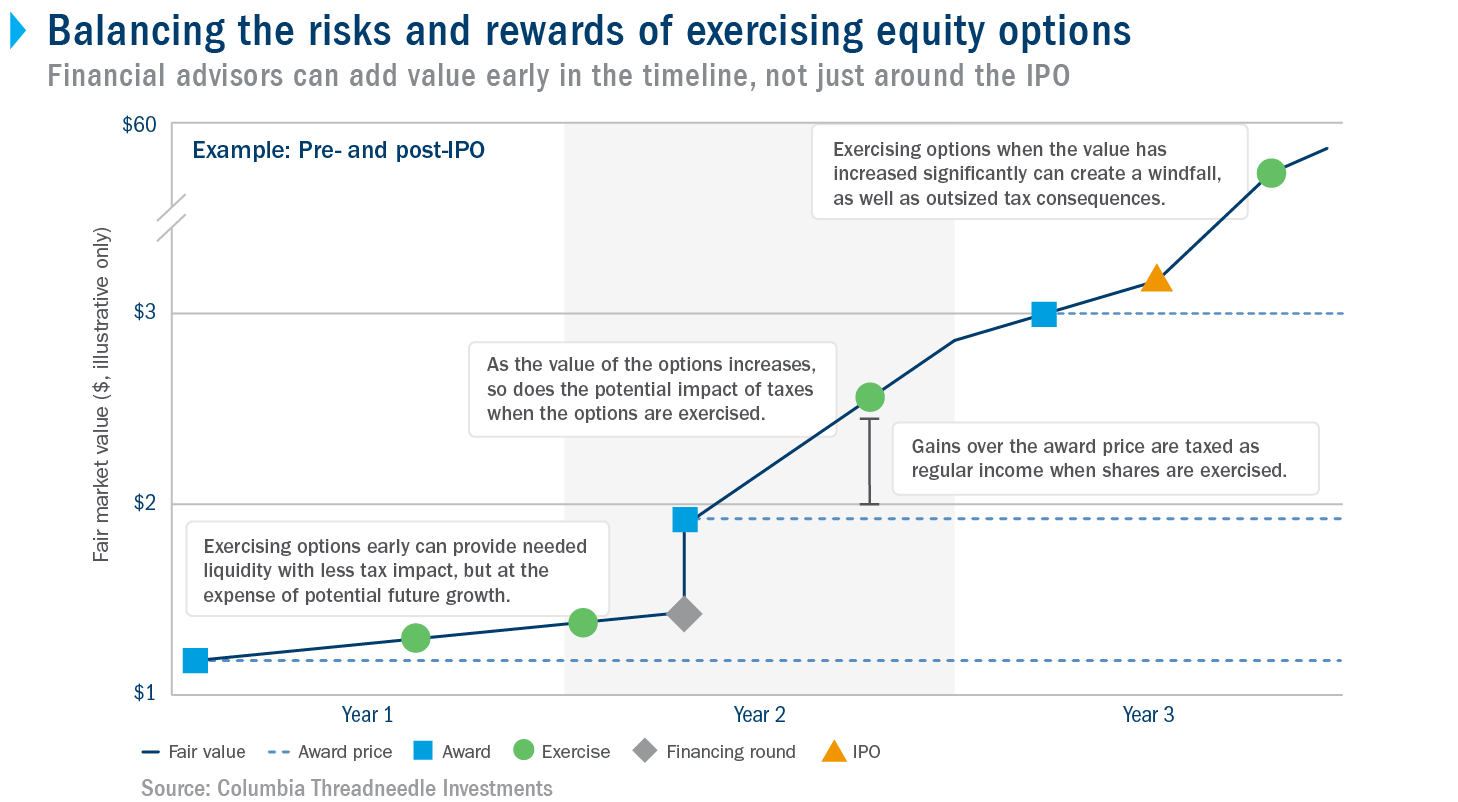

Clients who receive early options awards at pre-IPO companies need to determine if their employer permits actions, such as early exercise, that lock in lower taxes and improve the future tax posture when the stock is sold.

Even without early provisions, clients with pre-IPO equity compensation may need to be reminded to consider acting on vested options when the tax impacts may be lower — which means keeping track of the stock price and upcoming funding rounds.

The other end of the spectrum: Equity compensation at public companies

Back in the 1980s, stock options were the most common type of equity compensation. Nowadays, restricted stock units (or time-vested awards) are more common, as well as performance stock units (time- and performance-vested awards), which incentivize employees to remain at a company and hit certain success metrics.

But no matter what flavor, it’s still compensation that’s added to W2 income when the stock is acquired. For high earners, and especially executives, significant increases in income can bump them into higher tax brackets — a situation where tactical use of elective deferred compensation plans can help offset extra tax liabilities.

A common concern, particularly among clients who have amassed significant stock positions over long periods, is a lack of diversification. While they may blush at the tax bill when they exercise options or receive shares due to vesting restricted stock grants, diversifying those shares can be done without adding much, if anything, to the tax bill.

The bottom line

Starting a conversation about equity compensation with your clients can deepen your current relationships and lead to new opportunities to add value and gather assets. Clients who understand what they have through their equity compensation plan are better prepared to consider how it fits into their wealth strategies and are more eager to talk to someone who understands its nuances about their larger wealth management picture.

Leverage our equity compensation resources to help your clients build tax- and risk- aware strategies. Get started. |