Disclosures

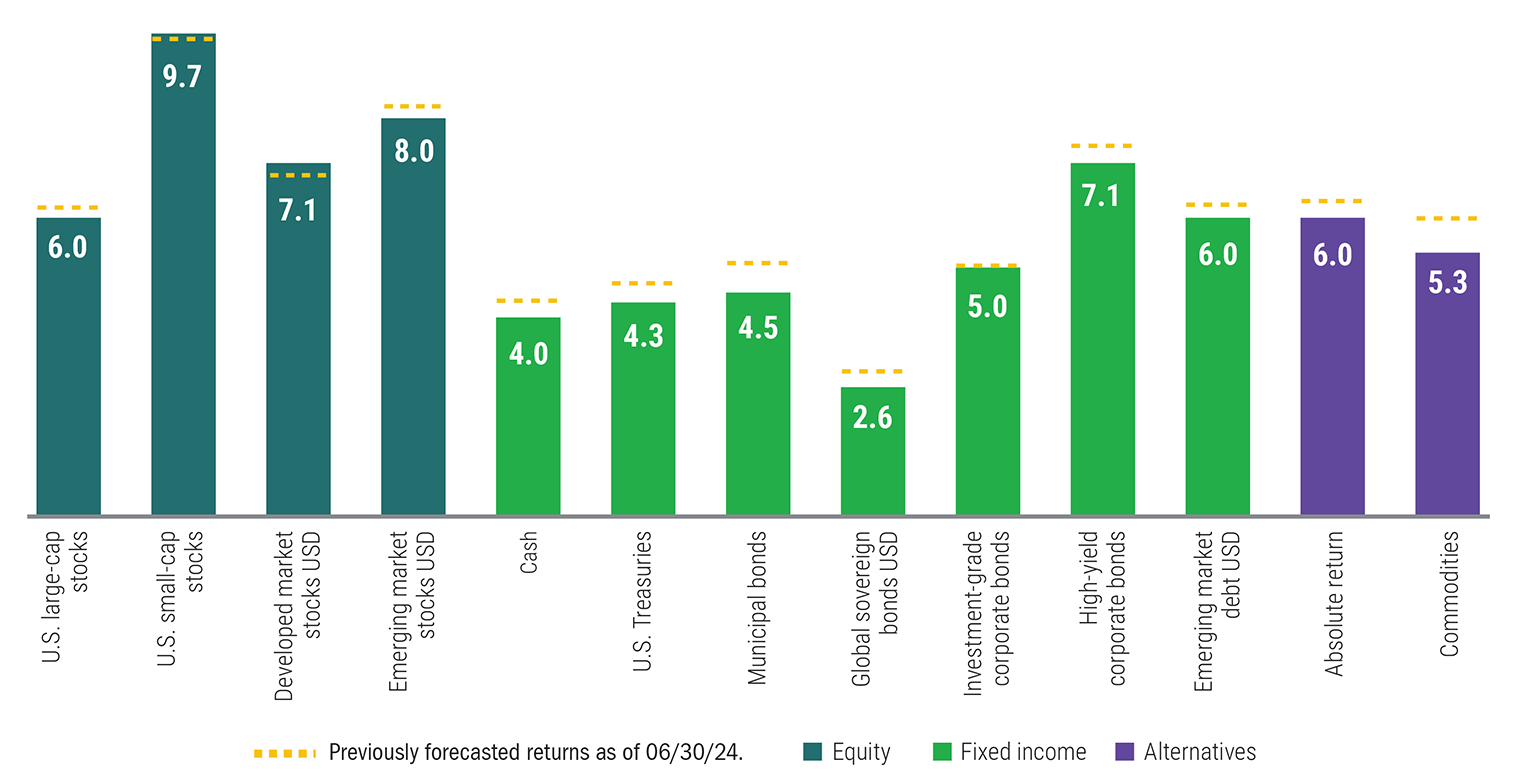

* Equity forecasts are based on three components: expected dividend payments, expected earnings growth and change in valuation levels (price-to-earnings ratios). Expected earnings growth is driven by expected economic growth, input cost changes and pricing power. Fixed-income forecasts are based on the shape of the yield curve, direction of interest rates, increase/decrease in yield spreads and timing of those changes. The major asset classes are based on the following indices: U.S. large-cap stocks (S&P 500 Index), U.S. small-cap stocks (Russell 2000 Index), Developed market stocks USD (MSCI EAFE Index), Emerging market stocks USD (MSCI EM Index), Cash (FTSE U.S. Domestic 3-Month T-Bill Index), U.S. Treasuries (Bloomberg U.S. Treasury Index), Municipal Bonds (Bloomberg Municipal Bond Index), Global sovereign bonds USD (Bloomberg Global Treasury Index (excl. U.S.), Investment-grade corporate bonds (Bloomberg U.S. Aggregate Credit Index), High-yield corporate bonds (Bloomberg Corporate High Yield Index), Emerging market debt USD (JPMorgan EMBI Global Diversified Index), Absolute return (FTSE U.S. Domestic 3-Month T-Bill Index, Commodities (Bloomberg Commodity Index).

The Standard & Poor’s (S&P) 500 Index tracks the performance of 500 widely held, large-capitalization U.S. stocks. The Russell 2000 Index measures the performance of the 2,000 smallest companies in the Russell 3000 Index, which represents approximately 8% of the total market capitalization of the Russell 3000 Index. The MSCI Europe, Australasia, Far East (EAFE) Index is a capitalization-weighted index that tracks the total return of common stocks in 21 developed-market countries within Europe, Australasia and the Far East. The Bloomberg Municipal Bond Index is considered representative of the broad market for investment grade, tax-exempt bonds with a maturity of at least one year. The Bloomberg U.S. Aggregate 1-3 Years Index is an unmanaged index of publicly issued investment grade corporate, US Treasury and government agency securities with remaining maturities of one to three years. Unlike mutual funds, indices are not managed and do not incur fees or expenses. It is not possible to invest directly in an index. The JPMorgan Emerging Markets Bond Index Global (“EMBI Global”) tracks total returns for traded external debt instruments in the emerging markets, and is an expanded version of the JPMorgan EMBI+. As with the EMBI+, the EMBI Global includes U.S. dollar-denominated Brady bonds, loans, and Eurobonds with an outstanding face value of at least $500 million. It covers more of the eligible instruments than the EMBI+ by relaxing somewhat the strict EMBI+ limits on secondary market trading liquidity. FTSE U.S. Domestic 3-Month T-Bill Index: FTSE 3-Month Treasury Bill Index is an unmanaged index that tracks short-term U.S. government debt instruments. Bloomberg U.S. Treasury Index: Bloomberg US Treasury Index represents the US Treasury component of the US Government index. Bloomberg Global Treasury Index: Bloomberg Global Treasury Index tracks fixed-rate local currency government debt of investment grade countries. The index represents the Treasury sector of the Global Aggregate Index and currently contains issues from 37 countries denominated in 23 currencies. The three major components of this index are the US Treasury Index, the Pan-European Treasury Index, and the Asian-Pacific Treasury Index, in addition to Canadian, Chilean, Mexican, and South-African government bonds. Bloomberg Corporate High Yield Index: The Bloomberg US Corporate High Yield Bond Index measures the USD-denominated, high yield, fixed-rate corporate bond market. Securities are classified as high yield if the middle rating of Moody’s, Fitch and S&P is Ba1/BB+/BB+ or below. Bonds from issuers with an emerging markets country of risk, based on Bloomberg EM country definition, are excluded. The Bloomberg Commodity Index Total Return (formerly DJ UBS Commodity Index), is a broadly diversified index composed of commodities traded on U.S. exchanges, with the exception of aluminum, nickel and zinc, which trade on the London Metal Exchange (LME). It is not possible to invest directly in an index.

Indices are unmanaged and not available for direct investment.

Diversification does not assure a profit or protect against loss.

For index descriptions, click here