- Our Blog

- White Paper

Download PDF

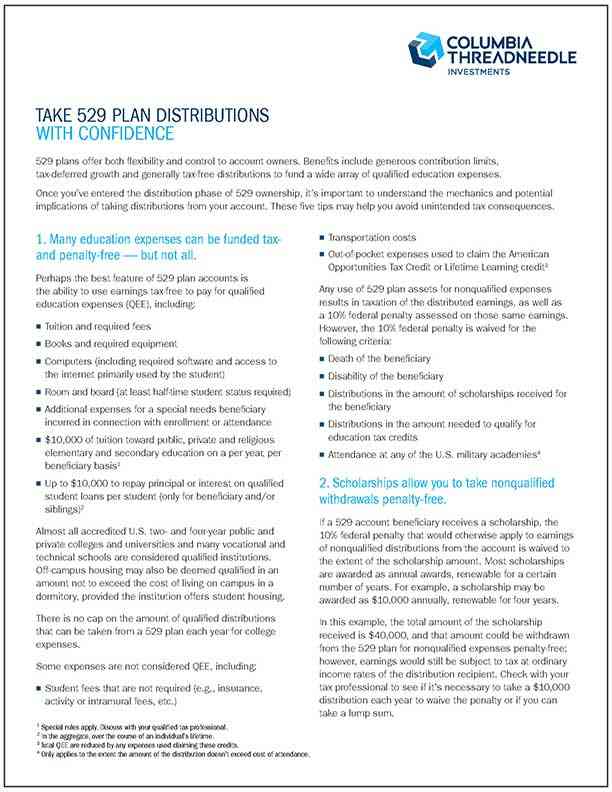

529 plan distributions can be confusing. And knowing how — and when — to take them can be critical for participants.

529 college savings plans are tax-advantaged accounts designed to pay for qualified education expenses, but the mechanics and implications of taking distributions from 529 plan accounts can be confusing. It’s particularly important to know the difference between qualified education expenses — which can be funded tax- and penalty-free — and non-qualified education expenses. Any use of 529 plan assets for nonqualified expenses could result in taxation of the distributed earnings, as well as a 10% federal penalty.

Our paper on the subject can help clear up confusion for 529 investors and beneficiaries, including explaining qualified and non-qualified expenses, tax form 1099-Q and how to think about timing of distributions. There has been meaningful progress for individuals with disabilities and their families with the development of 529A accounts, also known as ABLE accounts, which can be used tax-free to pay for any disability-related expenses.

Knowing how and when to take 529 plan distributions can be a critical consideration for participants. And understanding the mechanics and options can make for an easier experience with fewer tax consequences. Few financial vehicles provide account owners with as much flexibility and control as 529 plans, and fortunately those benefits extend to distributions.